Did We Already Reach Peak Software?

Set Trending Topics as a preferred source on Google.

Jennifer Martin is a Portfolio Specialist at T. Rowe Price. In this guest contribution, she examines a market rotation toward physical assets, pricing power, and direct engagement in AI – and away from companies whose value is heavily based on intellectual property or network effects.

We believe global equities are undergoing an AI-driven regime shift that breaks with the playbook common since the global financial crisis (GFC) of low rates, financial repression, and increasingly concentrated exposure to a small group of mega-cap technology companies and quality compounders. In that earlier regime, a focus on capital-light “compounders” and passive exposure to the largest index constituents was a rational response to scarce growth and abundant liquidity. Today, the situation is different. Higher nominal growth, persistent inflation risks, and rising investment in AI and infrastructure are shifting market preferences.

The market now rewards what you can touch. Capital is flowing toward companies with physical assets, pricing power, and direct engagement in AI and industrial expansion. Asset-light platforms and software models that once led the market are falling behind. This appears to be more than a short-term rotation. It reflects skepticism about AI monetization at the platform level, the recognition that value first flows to the “picks and shovels” of the AI cycle, and a reassessment of the premiums assigned to knowledge-based, asset-light business models.

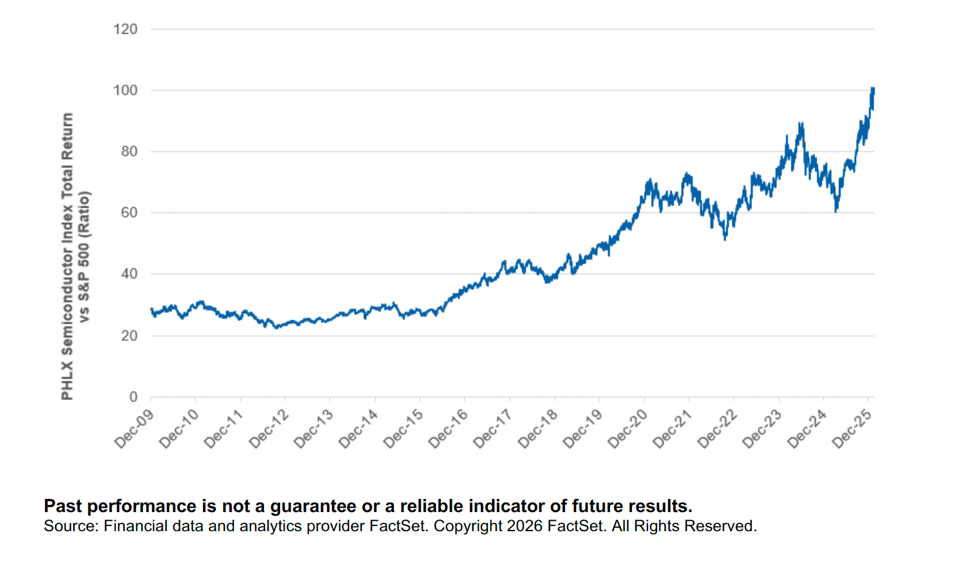

AI Investment Cycle Benefits Suppliers

We have identified four key dynamics shaping this environment: Material assets are commanding a premium. Industrial companies, energy producers, mining companies, utilities, and semiconductor fabricators – companies that build, extract, produce, and generate – are experiencing broad-based strength. In our broader observation universe, capital-intensive sectors show roughly 25% higher frequency of stocks at relative highs compared to capital-light sectors, which represents an unusually large differential in historical terms. These are companies whose competitive advantages rest on physical infrastructure, operational scale, and the ability to pass costs through in an inflationary environment.

Investors are rewarding companies whose value is based more on real assets than on intellectual property or network effects. This is happening precisely as early signs of a cyclical upturn are emerging, manufacturing activity is stabilizing, and order intake is increasing, further fueling the already strong trade in “real assets” by amplifying demand for industrial capacity and energy.

The AI investment cycle benefits suppliers, not consumers. The PHLX Semiconductor Sector Index (SOX) is near its relative all-time high versus the S&P 500, while AI picks-and-shovels companies continue to outperform. Meanwhile, some of the leading AI infrastructure investors are lagging.

Part of the problem is capital intensity: hyperscalers, once viewed as sustainable compounders, are now making extraordinary investments, with total AI and infrastructure investments consuming much of operating cash flow and driving some companies toward negative free cash flow. The market is treating these companies less like capital-light platforms and more like capital-intensive projects. Investors currently appear to prefer companies selling devices and components over those promising longer-term software monetization.

PHLX Semiconductor Index versus S&P 500 Index (December 31, 2009 – February 12, 2026)

Energy and commodities are experiencing a boom. This overlay of commodities and real assets reinforces the view that markets are pricing in persistent inflation, tighter physical supply chains, and the capital intensity required for the energy transition and infrastructure modernization. These sectors offer inflation protection and pricing power that asset-light models simply cannot match.

Software and platforms are being systematically downgraded. The S&P Software Index is in a sustained downtrend, correlating with general speculation fatigue, with a number of high-quality software franchises experiencing relative weakness. The underperforming group consists predominantly of capital-light companies with recurring revenue and high multiples, such as software/software as a service (SaaS), internet platforms, IT services, and financial data companies. These are precisely the areas that led in the previous cycle. Many of these companies remain fundamentally strong but face a dilemma: on one hand, rising discount rates and capital-intensive AI and infrastructure cycles are pulling capital toward real assets; on the other, AI itself threatens to undermine knowledge work and impair the economics of capital-light, fee- and placement-based models.

What Does This Mean for Positioning?

We believe this late-cycle, value-oriented rather than growth-oriented, tangible rather than intangible regime will persist until either inflation expectations decline significantly or asset-light sectors experience substantial valuation capitulation that creates compelling relative value. In the meantime, we continue to emphasize companies with physical assets, exposure to infrastructure and industrial expansion, and the ability to generate cash flow in an environment where capital is expensive and growth is scarce. This is not an environment for beta or story stocks. It is an environment that rewards fundamentals, cash flow generation, and assets you can see and touch. Key risks include a decline in hyperscaler AI spending that reduces infrastructure demand, a renewed surge in inflation that pressures all risk assets, sharp corrections in certain beneficiaries of real assets, or a return to a low-inflation regime in the post-global financial crisis style following a significant shock.

Other Sectors

Banks, tanks, and real assets: It is an unusual situation when industrials, energy, and consumer staples are among the year’s top performers (as of February 12, 2026). This reflects both the strength of the real assets and earnings trade and a shift in what investors currently view as “defensive,” while business services and other asset-light models lose that status. Portfolio positioning tends toward the “banks, tanks, and AI” regime, with elevated exposure to financials and industrials and growing emphasis on the energy sector, which benefits both from higher nominal growth and serves as a hedge against more persistent inflation.

Recapturing alpha from winners: We have systematically reinvested gains from high-momentum AI winners into high-quality, temporarily pressured names in areas such as payments, consumer staples, and selected cyclicals that remain consistent with our investment approach but offer different risk profiles.

Underweight Mag-7 stocks: As a group, we are underweight the Mag 7 as we see increasing dispersion in their AI strategies, investment intensity, and growth trajectories, and believe active stock selection in other areas offers a better risk-reward profile than owning the entire mega-cap group.